US - AI momentum overshadows and deepens labour weakness

The revision to labour market data brings it closer in line with sentiment. Core PCE inflation back at 3.0%, while CPI continues to slow to 2.5%. Headline GDP weaker than expected, but AI-investment fueled private demand holds up.

The past month saw a rollercoaster of data releases and policy announcements, echoing the first half of last year. GDP surprised to the downside, but private demand held up. Job gains surprised to the upside, and the unemployment rate even fell to 4.3%. Still, large negative revisions confirmed that almost no jobs were created over the past year. Meanwhile, January CPI inflation readings were surprisingly low, while December PCE inflation readings were surprisingly hot, with y/y core PCE picking up to 3.0%. On the policy front, Kevin Warsh was nominated to lead the Fed from June, and the Supreme Court finally decided to annul Trump’s emergency tariffs. This means that we’re set for another year of substantial policy uncertainty, with Warsh explicitly stating he thinks the Fed should give less guidance (see also our spotlight), and the Trump administration trying to find ways to reinstate tariff policy.

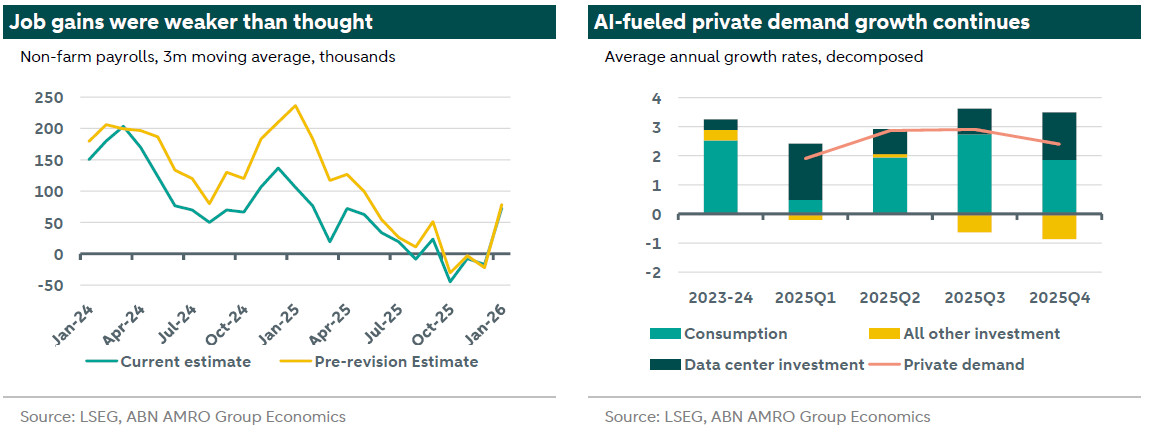

The jobs data revision did little to change our overall assessment of the labour market. The signal still shows that the labour market was stalling around the summer of 2024, with the 3m-average reaching around 50k a month, at a time where supply growth was substantially stronger. Most likely in response to the Fed’s easing, the labour market picked up, but the revised data shows the recovery was more short-lived than previously thought. Job gains declined again the minute the Trump administration took office, likely in response to the massive policy uncertainty. Markets predominantly reacted to the uptick in January rather than the overall downward revision. We think it’s a temporary blip, with gains still driven by a very concentrated labour market, as virtually all job gains in health care. We expect weaker figures in the coming months, predominantly on the back of lackluster supply, and some weakness in demand due to post-pandemic labour hoarding, and initial effects of AI adoption.

On the inflation front, January CPI inflation came in surprisingly cool, with the headline index rising by just 0.17%, compared to an average January reading of 0.45% over the past three years. This led to a sharp decline in the y/y rate to 2.4%. Not helped by a windfall from energy prices, core increased by 0.3%, with the y/y dropping to 2.5%. Goods inflation was mostly flat, but bifurcated. Recreational goods rose in price, while used cars fell. Price increases in recreational goods can be explained by the AI investment boom, which is causing shortages in various inputs to e.g. consumer electronics. Core services came in strong at 0.4%, particularly in discretionary services such as airfares. This is likely demand-driven inflation, on the back of substantial wealth effects accumulated over the past year.

Finally, the US economy grew at 1.4% annualized in the fourth quarter, slowing from 4.4% growth in the third quarter. That puts total growth for 2025 at 2.2%. The BEA suggested the government shutdown, which lasted almost half the quarter, subtracted about 1%. This should mostly unwind in the first quarter of this year. Indeed, Federal government spending decreased by more than 15%. The contribution from net exports was minimal, where a positive impact was expected until December trade data was released, which showed one of the largest full-year deficits on record, after a notably volatile trade year. Private demand still rose at a solid 2.4%, as consumer spending cooled down to 2.4%, from 3.5% prior, while business investment grew at a solid 3.7% pace, again mainly reflecting the AI spending boom. All other investment showed a continued contraction. The overall 2025 contraction of 0.4% is the worst since the great financial crisis. Still, we expect AI spending, along with monetary and fiscal stimulus, to continue to be a driver of growth and inflationary pressures in the coming year. The supreme court decision to annul Trump’s emergency tariffs adds new uncertainty, but seems unlikely to materially effect the outlook.