Implications of Middle East escalation

The military escalation in the Middle East threatens the economy because of the disruption to energy supplies and increased uncertainty. Energy infrastructure has not yet been significantly impacted, but that remains a risk as air strikes continue to rage. Shipping through the Strait of Hormuz - one of the world's most important energy choke points - has come to a near stand-still. Any sustained energy price shock would have more noticeable effects on inflation than growth. We present inflation scenarios assuming oil at USD 80 per barrel, 100 and 130; in all cases inflation spikes in 2026 but falls back in 2027 . For monetary policy, the duration of the shock is crucial, as are second round effects, given the focus on the medium term.

Introduction

Over the weekend, the US and Israel conducted air strikes on Iran. Iran retaliated with strikes across the region, and shipping through the Strait of Hormuz came to a near stand-still. The military escalation in the Middle East represents yet another ramping up of geopolitical risks for the economy and financial markets. The main transmission channels come from the disruption of energy supplies and increased uncertainty. With uncertainty high about what happens next, we try to shed some light on the possible macro implications.

Energy supply and transportation at risk

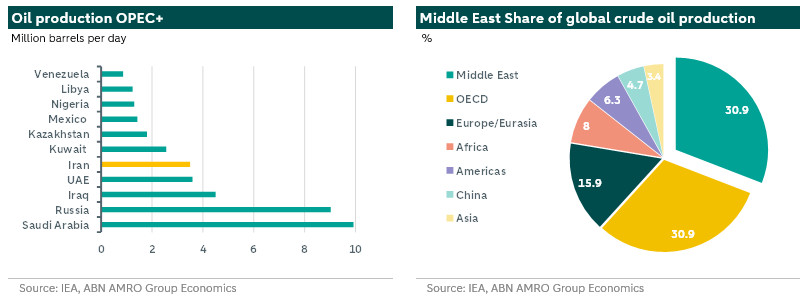

To start with energy supply, there are threats to both production and transportation. The Middle East contains five of the world’s top-ten oil producing countries (Saudi Arabia, Iran, Iraq, United Arab Emirates and Kuwait) and three of the top-ten natural gas producers (Iran, Qatar and Saudi Arabia). It is responsible for around a third of global oil production and around a quarter of global natural gas production.

Meanwhile, the strait of Hormuz - between Iran and Oman - is one of the world's most strategically important energy choke points. Flows through the Strait of Hormuz (around 20m barrels per day) make up around a quarter of total global seaborne oil trade and around a fifth of global LNG trade, mainly from Qatar. The alternatives are limited - for instance, the EIA estimates that about 2.6m barrels per day of capacity from the Saudi and UAE pipelines could be available to bypass the Strait.

So far, the military escalation does not seem to have significantly damaged energy infrastructure, though it has severely impacted traffic through the Strait of Hormuz. According to Reuters, a number of ships have come under fire, and several tanker owners, oil majors and trading houses have suspended crude oil, fuel and liquefied natural gas shipments via the Strait. Indeed, data from MarineTraffic suggests flows have dried up.

Asia most vulnerable, but price impacts are global

The EIA estimates that more than 80% of the crude oil and LNG that moves through the Strait of Hormuz goes to Asian markets, with very modest amounts going to the EU and US. Having said that, all economies would be impacted by the disruption via higher prices.

Oil and gas prices surge

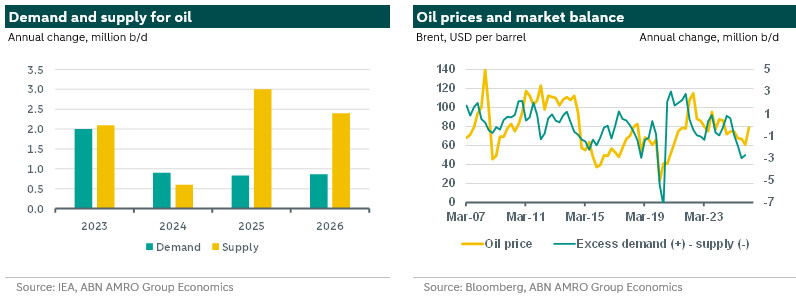

Energy prices had already been moving up before the weekend. At market close on Friday, Brent oil prices had built in a risk premium related to potential military escalation of around USD 7 per barrel, with prices closing at just below USD 73. Oil prices predictably jumped at open this week, with Brent at USD 79 at time of writing. Benchmark gas futures prices, which had been subdued in the run-up, have surged and stand about 20% higher.

Possible energy shocks

The eventual impact on energy prices and hence on the outlook will obviously depend on how the conflict evolves. There are a number of potential shocks that could be impactful. One - which is already materialising - is the blocking of the Strait of Hormuz. The general consensus among military and security analysts seems to be that this is unlikely to last long (days/weeks rather than months) because of the military capabilities of the US.

In addition, it is not in Iran’s interest to continue blocking the Strait. Its own oil exports flow through the Strait, while China – the largest single destination for oil through the Strait – would also likely add pressure on the Iranian authorities. Still, even assuming that a full closure will be short, Iran could potentially make traffic more difficult for longer.

In addition, there could be a disruption of Iran’s own oil supplies, either through strikes or through the US restricting Iran’s shipments (around 1.6m barrels per day). Damage to supply would likely have a bigger price impact because it would likely take longer for production to come back on stream. Finally, there is the risk that Iran attacks the oil infrastructure in other countries in the region. Depending on which infrastructure in which countries, this is the shock that has the potential to trigger a surge to historically-high prices.

Potential cushions

There are potential cushions. First, the oil market was well supplied, with the IEA projecting that supply would far exceed demand this year. Second, OPEC+ decided over the weekend to increase oil production by 206K barrels per day in a (likely in vain) bid to calm markets. Third, oil consumers have strategic stocks that they hold for emergencies. The US has indicated that it is not currently considering releasing oil from its strategic petroleum reserves, suggesting it does not see the need at this stage.

Bigger impact on inflation than growth

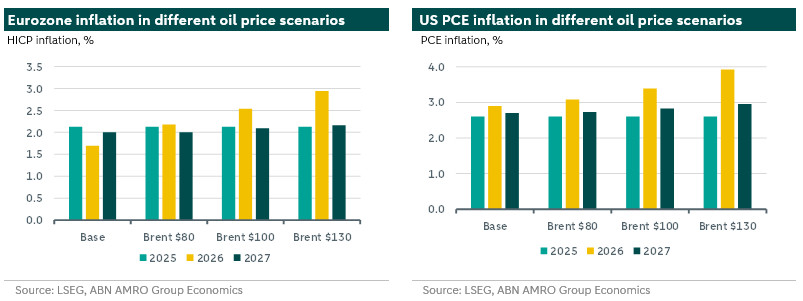

A rise in energy prices typically leads to bigger impacts on inflation than on economic growth. The impact on inflation naturally depends on the magnitude and length of the oil price shock. Below we show three inflation scenarios: Brent at $80, $100 and $130 per barrel, with the price shock persisting to end-2027. Already facing above target inflation, higher oil prices put the Fed in an even more difficult situation. Headline inflation will rise substantially, while core inflation, which excludes energy prices, barely moves. The usual policy response, which remains the most likely for now, is therefore to look through the oil price shock, seeing as it’s a one-off inflationary impulse. In the current setting, things are more complicated, because the scenario of oversupply with falling energy prices provided a tailwind in headline inflation, which could be used to argue in favour of rate cuts. Higher energy prices, and a resurgence of inflation, could very well tilt the already fragile balance in the FOMC towards holding rates, on the fear of inflation expectations becoming de-anchored, even if the shock is temporary. For our base case to alter, we would need to see, or expect, sustained higher oil prices. Signs of inflation de-anchoring would put a nail in the coffin for rate cuts this year.

Turning to the eurozone, in the mildest scenario (Brent $80), inflation goes from being well below the ECB’s 2% target to moving broadly back to target and staying there. Even in the most severe (Brent $130) scenario, while eurozone inflation is boosted by 1.3pp in 2026, the lasting impact is relatively mild, with 2027 inflation only 0.2pp higher.

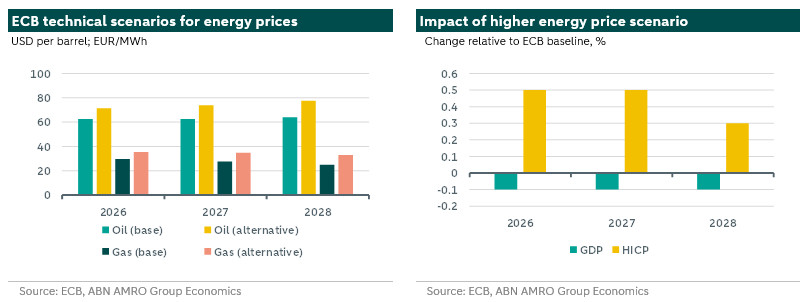

In its last set of projections in December, the ECB also published alternative scenarios for growth and inflation based on a higher energy price scenario than it assumed (see charts). Under this scenario, inflation would be 0.5% higher in 2026 and 2027 and 0.3% above its baseline in 2028, whereas economic growth would be only 0.1% lower in each year. This would leave inflation above its target compared to close to target and therefore would raise the prospect of early ECB rate hikes.

However, this is a scenario that assumes that high oil prices will sustain in the coming years. The scenario we are heading towards is more likely to be one where oil prices jump more than the ECB’s scenario in the near term (indeed they already have), but then come down more sharply later in the year. This would then imply upward revisions to 2026 inflation forecasts, but more modest changes to 2027-2028. The ECB’s view on the duration of the shock and potential second round effects, on for instance wages, would drive how minded it is to hike interest rates. We judge however that even in the most severe scenario, significant second round effects (as during the energy crisis) are unlikely, as the impact of such a rise in oil prices is much less than what we saw with the surge in gas prices back in 2022 (which pushed inflation into double digits). As far as the impact on economic growth is concerned, the direct effects could potentially be magnified by heightened uncertainty, which could make consumers and businesses more cautious. It is currently too early for us to make any changes to our own base case.