Housing Market Monitor - April 2025 - Summary

We maintain our price forecast, with+ 7% price growth in 2025 and+ 3% in 2026. We increase our transaction growth forecast for 2025 to +5% (was +2.5%). The drivers remain rising wages, lower mortgage rates and the supply shortage.

2024 showed a robust price growth.

After a weak year in 2023, house prices grew strongly again in 2024, with an average price increase of 8.7%. Prices thus reached new record levels. The main drivers were falling mortgage rates, the supply shortage and higher household incomes. , leading to a 3% increase in real disposable income, the income that households feel the most. It appears that much of the extra income from previous years was invested in housing, as total Dutch mortgage debt increased by 35.7 billion euros through 2024. But as a percentage of GDP, mortgage debt fell and reached its lowest level in more than 20 years. One reason is that many homes are less debt-financed than they used to be. This is due to tighter lending standards (lower LTV standard, fewer repayment-free mortgages), leading to a better financial situation for homeowners. Therefore, we see no signs that the high home prices are leading to financial problems for (new) homeowners.

Liquidity rose especially for apartments.

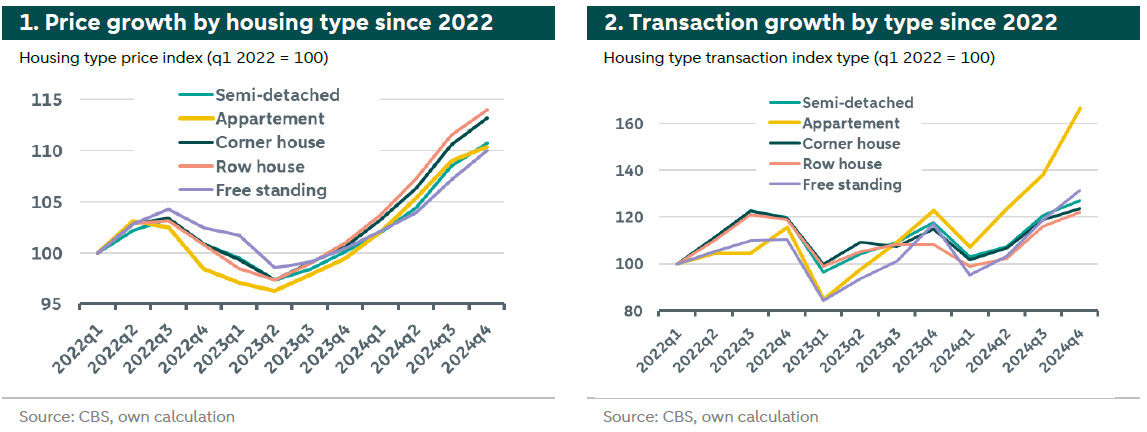

Not only did prices rise, but liquidity rose as well. The number of transactions exceeded 200,000 for the first time since 2022. This shows that buyers were eager to buy and sellers were eager to sell again. Among the sellers were also many private investors who decided to sell their properties, mainly due to new tax regulations and the Affordable Rent Act. Figure 1 shows the price trend and Figure 2 the transaction trend by housing type since 2022. In Figure 1, we see differences in the price development of different housing types, although they are not very large. Intermediate houses showed the highest price growth, while detached houses showed the lowest price growth. Looking at Figure 2, we see a clear differentiation for apartments though, showing strong transaction growth in 2024. Apartment transactions in the fourth quarter of 2024 were 60% higher than in the first quarter of 2022.

Our price estimates remain unchanged, but we expect slightly more transactions in 2025.

With a robust year behind us and trends being unchanged, we expect price growth to continue in 2025. We therefore maintain our latest forecast of +7% price growth for 2025 and +3% for 2026. We expect price growth to be driven mainly by the and rural areas. In contrast, we expect price growth in Amsterdam, Rotterdam and The Hague to be just below the expected average. We are further raising our transaction forecast for 2025 and expect an increase of +5% (was +2.5%). We continue to see high liquidity in the market and expect sales by private investors to continue until the end of 2025. From 2026, we expect the wave of sell-offs to be over. Therefore, we leave our transaction growth estimate for 2026 unchanged at +1%.

Trends suggest that housing demand remains stable.

We see an increase in household income in 2024. This supports our expectations for more demand in 2025, as we typically see a lag between income increases and prices. Labor market tightness and collective bargaining agreements further suggest that household income will continue to rise in 2025. Furthermore, we expect mortgage rates to fall, even though the bottom is near. The European Central Bank (ECB) is expected to further reduce its deposit rate, which is a benchmark for mortgage rates. However, risk premiums are rising slowly, so lenders will struggle to pass on all of the ECB's interest rate cuts. We therefore expect mortgage rates to bottom out in late 2025, early 2026.

On the supply side, we see few signs of improvements for 2025.

Recently, we have seen an uptick in construction activity, which is a good sign. However, we do not think it will be enough to drive down prices in 2025. Overall, current construction activity is below the level needed to reduce the supply shortage. At the end of 2024, Minister Keijzer invited a housing summit to discuss improvement ideas and make construction agreements, but so far little to no concrete action has followed. We think that among all the bottlenecks, such as energy grid expansions and nitrogen, the biggest problem is the lack of investors to fill a sustainable pipeline. It seems investors especially lack planning stability. Consequently, a recent to roll back the Affordable Rent Act was criticized as it would once again saddle investors with uncertainty about the government's direction. Therefore, we do not expect a nearby price drop due to supply.

Despite a turbulent start in 2025, we do not yet expect major trend changes.

Finally, we do not want to ignore the signs of headwinds in the housing market at the beginning of 2025. Mortgage rates rose slightly and monthly price growth nearly came to a halt in February. However, the rise in mortgage rates can be partly explained by the relaxation of the German debt brake and the green light for nearly 1 trillion euros of new debt. This adds risk to the euro zone, causing mortgage rates to rise slightly. But part of the recent rise can also be explained by uncertainty about President Trump's tariff plans for EU goods.[1] However, we estimate the impact on the Dutch housing market to be small and expect it to take a long time before the economic effects (if any) become apparent. Therefore, we maintain our expectation despite these developments.

[1] At the time of writing (late March), "Liberation day" tariffs were not yet known.