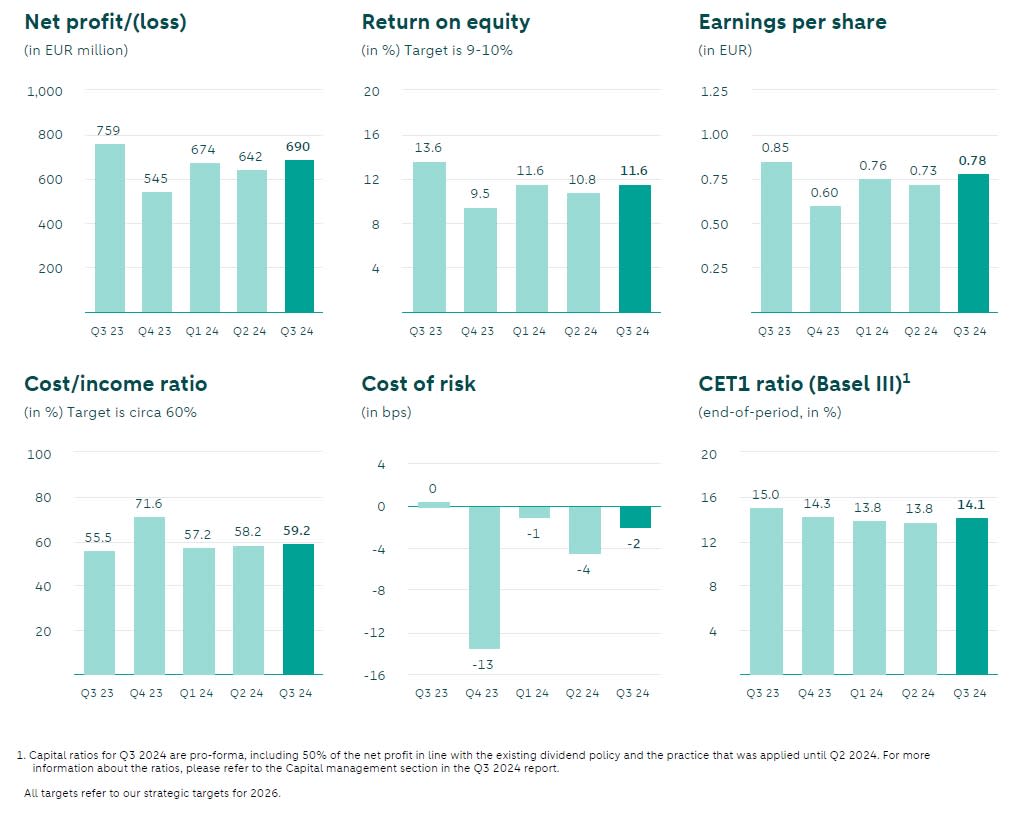

ABN AMRO Bank posts net profit of EUR 690 million in Q3 2024

;%20}%20.cls-2%20{%20fill:%20url(%23linear-gradient-2);%20}%20.cls-3%20{%20fill:%20url(%23linear-gradient-4);%20}%20.cls-4%20{%20fill:%20url(%23linear-gradient-5);%20}%20.cls-5%20{%20fill:%20url(%23linear-gradient);%20}%20%3c/style%3e%3clinearGradient%20id='linear-gradient'%20x1='8.089'%20y1='-4.628'%20x2='8.089'%20y2='17.703'%20gradientTransform='matrix(1,%200,%200,%201,%200,%200)'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0'%20stop-color='%23005eff'/%3e%3cstop%20offset='1'%20stop-color='%2300b2ff'/%3e%3c/linearGradient%3e%3clinearGradient%20id='linear-gradient-2'%20x1='12.007'%20x2='12.007'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-3'%20x1='12.007'%20x2='12.007'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-4'%20x1='15.926'%20x2='15.926'%20xlink:href='%23linear-gradient'/%3e%3clinearGradient%20id='linear-gradient-5'%20x1='12'%20x2='12'%20xlink:href='%23linear-gradient'/%3e%3c/defs%3e%3cpolygon%20class='cls-5'%20points='6.413%209.134%206.413%2015.125%209.765%2012.129%206.413%209.134'/%3e%3cpath%20class='cls-2'%20d='M12.492,13.663c-.302,.255-.747,.248-1.04-.018l-.698-.632-3.062,2.737h8.631l-3.062-2.737-.769,.649Z'/%3e%3cpolygon%20class='cls-1'%20points='16.613%208.25%207.402%208.25%2012.007%2012.366%2016.613%208.25'/%3e%3cpolygon%20class='cls-3'%20points='17.601%2015.125%2017.601%209.134%2014.25%2012.129%2017.601%2015.125'/%3e%3cpath%20class='cls-4'%20d='M19,2H5c-1.66,0-3,1.34-3,3v14c0,1.66,1.34,3,3,3h14c1.66,0,3-1.34,3-3V5c0-1.66-1.34-3-3-3Zm0,14.08c0,.51-.41,.92-.92,.92H5.92c-.51,0-.92-.41-.92-.92V7.92c0-.51,.41-.92,.92-.92h12.16c.51,0,.92,.41,.92,.92v8.16Z'/%3e%3c/svg%3e)

ABN AMRO Bank posts net profit of EUR 690 million in Q3 2024

Q3 Key messages

Strong quarterly results: Net profit of EUR 690 million and 11.6% return on equity, driven by improved net interest income, strong fees and net impairment releases

Continued mortgage portfolio growth: Supported by an increase in new clients, mortgage book grew by EUR 1.6 billion

Improved net interest income: Benefitted from better Treasury result driven by the favourable interest rate environment

Fee and commission income increased: Growth of 6% year-to-date compared with the same period last year, driven by good performance in all client units

Costs remain under control: Increase in costs as anticipated due to the start of our new collective labour agreement and upscaling of resources

Solid credit quality: EUR 29 million in net impairment releases, reflecting a low cost of risk

Strong capital position: Basel III CET1 ratio of 14.1% and Basel IV CET1 ratio of around 14%

Assessment of capital positionand potential room for share buyback postponed to Q2 2025 results

Robert Swaak, CEO:

“In the third quarter, ABN AMRO delivered another strong set of results with improved net interest income (NII), increased fee income and net impairment releases.

The resilient Dutch economy and thriving housing market continued to benefit our results. The rebound of the Dutch housing market was sustained in the third quarter, driving prices to new record levels. The average house price, as published by Statistics Netherlands, was around 4% higher than in Q2 2024 and around 11% higher than in Q3 2023. Transaction volumes have also continued to rise, with 15% more transactions this quarter compared to last year. Unemployment in the Netherlands is still historically low and the labour market remains tight. Inflation in Europe is continuing its downward trend, which is expected to drive the ECB to further interest rate cuts.

We saw our mortgage book grow by EUR 1.6 billion this quarter and year-to-date we remain market leader in new production. Our focus on the starters’ market resulted in an increased client base and a leading market share position in this segment. Our corporate loan book remained stable. In the transition themes new energies, digital and mobility, we continued to see growth in the Netherlands and Northwest Europe.

Our financial results were again strong during the third quarter. Net profit was EUR 690 million, resulting in a return on equity of over 11%. Net interest income increased to EUR 1,638 million, reflecting an improvement in our Treasury result, which benefitted from the favourable interest rate environment. Our fee income was strong, driven by higher payment services fees within Personal & Business Banking, higher asset management fees at Wealth Management and higher transaction volumes at Clearing and Global Markets. Costs were impacted by our new collective labour agreement which became effective as of 1 July and by further upscaling of our resources for data capabilities and regulatory programmes. We still expect full year costs to be around EUR 5.3 billion.

The resilient macro environment, low unemployment and the high credit quality of our portfolio led to limited inflow of individual impairments. These were offset by the impact of a new model with enhanced data for the mortgage portfolio, resulting overall in another quarter of net impairment releases. Our risk-weighted assets (RWAs) decreased by EUR 2.5 billion, mainly due to business developments and the first effects of data quality improvements. Together with the increase in CET1 capital, this resulted in a Basel III capital ratio of 14.1%. The Basel IV ratio remained around 14%. We are in the process of simplifying our model landscape while at the same time preparing for the upcoming implementation of Basel IV. Implementing these complex regulatory changes is taking longer than anticipated and as they impact our planned Q4 capital assessment, we have decided to postpone this assessment to Q2 2025.

We continue to work on enhancing customer experience and future-proofing our bank. Our clients are able to use a new feature in the ABN AMRO app to instantly verify whether an incoming call is genuinely from a bank employee. BUX announced a cooperation with PrimaryBid and Euronext, enabling our clients to participate in IPOs and other regulated fundraises, including deals previously reserved for institutional investors. This quarter, we were recognised by several external parties for our continued client focus and customer experience. Independent parties awarded us for our active client management and product offering in mortgages. Our ABN AMRO ODDO BHF joint venture was voted Best Benelux Broker in the 2024 European Ranking for the third year in a row. Our efforts in cyber security were recognised in our BitSight score, where ABN AMRO remains the industry leader in the Netherlands, with higher security ratings than its peers.

We remain focused on fulfilling our role in society, supporting our clients in the transition to a sustainable economy, with expertise on new business models and technology. In the last quarter we announced the financing of the construction of two large-scale biomethane plants in the Netherlands. This is also in line with the aim of the new Dutch government to increase innovative private financing for the climate and energy transition by a ‘green financial sector’. As part of ABN AMRO’s climate strategy, we are investing a total of EUR 1 billion in early-stage capital through direct equity investments, fund investments and hybrid capital investments. This quarter, our Sustainable Impact Fund invested in Blume Equity, a female founded and managed climate-tech growth investor, which is in line with our commitment to support female entrepreneurship. We also continue to invest in sustainability expertise. Together with the University of Amsterdam, we have launched a new Wealth Management training programme to ensure our employees continue to support our clients in the sustainability transition.

I am delighted that Serena Fioravanti joined us as CRO as of 1 October. I am confident that, with almost 25 years of experience in the banking sector and a highly relevant risk management track record, she will be successful in this role. I would like to thank Caroline Oosterloo-van 't Hoff for filling in the interim CRO position and I am looking forward to continue working with her as a senior leader in the risk organisation.

As always I would like to thank our clients for putting their trust in us while we continue to focus on being their preferred partner. And finally a continued recognition of the commitment and passion of all of our colleagues, enabling us to consistently execute our strategy.”